In the evolving landscape of digital payments, both contactless payments and mobile wallets have emerged as convenient and secure alternatives to traditional payment methods. Although often used interchangeably, these two payment technologies are distinct in terms of how they function and the specific tools they use to facilitate transactions. As...

How to Make Your Business Ready for Contactless Payments

In today's fast-paced and digital world, contactless payments have become increasingly popular among consumers. With the rise of mobile wallets and the convenience they offer, businesses need to adapt to this new payment method to stay competitive. This comprehensive guide will walk you through the process of making your business...

Advantages and Disadvantages of Contactless Payments

Contactless payments have become increasingly popular in recent years, offering a convenient way to conduct transactions with a simple tap. As technology continues to evolve, the ubiquity of these payment methods is becoming more pronounced in daily transactions around the globe. This article delves into the advantages and disadvantages of...

The Growing Popularity of Contactless Payments: How Businesses Can Embrace and Implement the Technology

Introduction to Contactless Payments Are you tired of fumbling for cash or swiping your card every time you make a purchase? Say hello to the future of payments – contactless technology! With just a tap or wave, businesses and customers alike are embracing the convenience and speed of contactless payments....

What Is a E-Wallets and How Does It Work?

An e-wallet is an electronic account where you store money, analogous to a physical wallet. It allows you to buy or sell goods and services online just like a traditional bank does — but without the brick and mortar, and with fewer fees. You can also use it at ATMs...

ACH vs EFT: What’s the difference?

ACH stands for Automated Clearing House, an electronic payment system used to transfer funds electronically. EFT stands for Electronic Funds Transfer, which is a generic term that typically refers to payments made using ACH. Technically speaking, however, ACH falls under the larger umbrella of EFT. The distinction between ACH and...

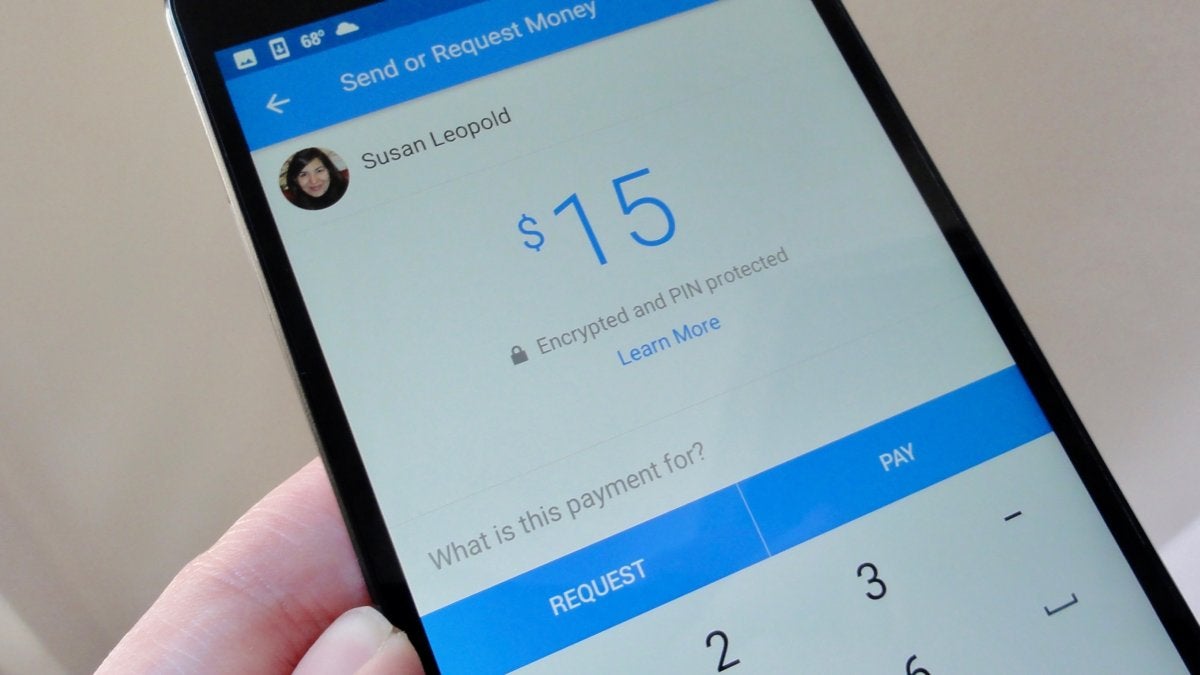

What is Facebook Pay?

Facebook has found a way to increase user engagement and time spent on their website by introducing Facebook Pay. Facebook users are able to send money in Messenger using debit cards or PayPal, however Facebook is now offering an in-app quick payment system that allows for instant transfer of funds...

What is Tap and Pay (NFC)?

Tap and Pay, also known as NFC (near field communication), is a technology that allows you to make contactless payments with your smartphone. With Tap and Pay, you can simply hold your phone up to a contactless payment terminal and the payment will be processed automatically. How does Tap and...